From next month, the maximum amount a RBS customer can rack up in bank charges each month tumbles from a staggering £6,688 to £260. Rupert Jones reports

There was good news for millions of current account holders this week when Royal Bank of Scotland and its NatWest arm announced they are slashing their overdraft fees.

The changes could save some people hundreds of pounds a month, and the move has prompted speculation about whether the other banks will follow suit.

RBS-NatWest is 70% owned by the taxpayer and has 12.5 million current account holders. The website uSwitch.com calculated that as a result of the cuts, the most someone could rack up in charges each month will tumble from a breathtaking £6,688 to "just" £260.

The lower charges will certainly make life easier for customers who go overdrawn without permission or who exceed their agreed overdraft limit.

These are the main changes, taking effect from 1 October:

• The "unpaid item fee" – imposed when a cheque, direct debit or standing order bounces – is being cut from £38 to £5. The maximum amount customers can pay in unpaid item fees will fall from £114 a day to £50 a month.

• The fee for paying for an item when someone is overdrawn (the "paid referral fee") will be cut by half to £15 a day.

• The "guaranteed card payment fee" (where a customer guarantees a payment by using a debit card with cheque guarantee facility) will be reduced to £15 from £35. This fee will be capped at £90 a month – down from £105 a day.

• The monthly maintenance charge for going overdrawn without consent is going down from £28 to £20.

• The unauthorised overdraft rate on standard accounts is being cut from 29.84% to 19.24% EAR.

The lower charges come as the test case on unauthorised overdraft costs continues to wind its way through the courts. The case has been brought by the Office of Fair Trading against seven banks and one building society, and questions the fairness of the fees they impose when someone exceeds their agreed borrowing limit.

The case is being heard by the House of Lords. An announcement is expected within weeks, and if the decision goes against the banks, it will pave the way for a further hearing to decide whether the charges are fair and, if not, what a fair charge would be.

Brian Hartzer, the new head of RBS's retail division, says: "This is good news for customers. As we look ahead, there are many issues to consider, but we thought it was time to move this particular customer concern forward by cutting our charges. We are changing what we do as a bank and the way we do it."

Some commentators speculate that RBS's move indicates it thinks the banks will lose the case. Or it could simply be that the state-controlled banking giant is bowing to political pressure, says Martin Lewis, the man behind MoneySavingExpert.com. He adds that a more cynical view is that banks can see the writing on the wall, and by saying they have fixed the "unfair bank charges" problem, they will negate any moves to regulate the system and avoid retrospective payouts.

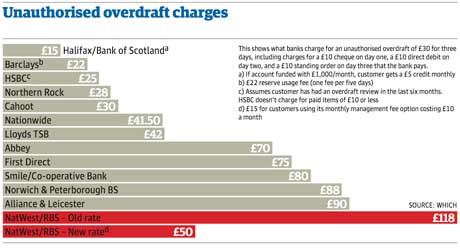

Others reckoned the announcement might be linked to claims in this month's Which? magazine that RBS customers were being hit with the highest unauthorised overdraft charges on the high street, with fees of £118 for a three-day overdraft.

Most of the major banks have made changes to their unauthorised overdraft fees over the past 12 months, "which suggests they are struggling to prove these fees are fair", says Ian Williams at Moneysupermarket.com. In August 2008, Barclays cut its overdraft fees as part of a shake-up which saw it launch "Personal Reserve" – designed as a safety net for customers who exceed their overdraft limit.

uSwitch.com calls RBS's move a brave one, which could be a lifeline for those struggling to keep their heads above water. "However, this shouldn't become a green light for customers to become sloppy when managing their current account," it adds.

Williams says the best advice is to avoid unauthorised overdrafts. For most people, this means a simple call to their bank. "If you do continually go into the red, then consider switching to a more competitive current account, such as one from Alliance & Leicester, which has a 0% interest rate for 12 months and will only charge 50p per day, maximum £5 per month thereafter on authorised borrowing," he adds.

But A&L – now part of Santander – is not so hot when it comes to unauthorised overdraft charges, according to the Which? report. The consumer body used the same scenario to compare all the main banks, and A&L was found to have the second-highest charges at £90. Smile and the Co-operative Bank would charge £80, and First Direct £75.